All translations on this site are unofficial and provided for reference purpose only.

To view translations, select English under Step 1 (at the right of the screen). Not every item is (fully) translated. If you’re still seeing Chinese, you can use machine translation, under Step 2, to make sense of the rest.

Want to help translate? Switch to English under Step 1, and check ‘edit translation’ (more explanation in the FAQ). Even if you translate just a few lines, this is still very much appreciated! Remember to log in if you would like to be credited for your effort. If you’re unsure where to start translating, please see the list of Most wanted translations.

Trial measures for the regional integration of central government State Owned Enterprises in the coal fired power sector

Original title: 《中央企业煤电资源区域整合试点方案》

Links: Source document (in Chinese): Original scans of the document were removed from most outlets a few days after posting. They are included for reference now at the bottom of this page.

Trial measures for the regional integration of central government State Owned Enterprises in the coal fired power sector

Since 2016, due to the combination of factors such as the rapid rise in coal prices, overcapacity of coal power, and intensified market bidding, the production and operation of coal power companies got into severe difficulties. Some enterprises are operating on a loss for years, the capital flow is broken, and production and operation are difficult to sustain.。In order to implement the decision of the Central Committee of the Party and the State Council on the deployment on deepening structural reforms of the supply side, the reduction of coal power generation capacity of central enterprises and the integration of regional resources should be accelerated and the healthy and sustainable development of the coal power industry promoted.。

1. Basic situation

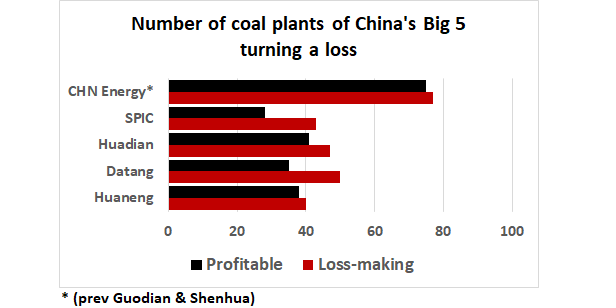

The SOEs of the central government that are involved in the coal-fired power sector are primarily the 5 companies China Huaneng, China Datang, China Huadian, the State Power Investment Corporation (SPIC) and CHN Energy [a merger of Guodian and Shenhua] (the State Development Investment Corporation (SDIC)), China Resources Group, the China National Coal Group and other SOE also have coal-fired power assets)。As of December 2018, these five companies owned a total of 474 coal-fired power plants, with a total generation capacity of 520 GW, representing total assets of 1500 billion RMB, and total liabilities of 1100 billion RMB, or an average debt-to-asset ratio of 73.1%, of which:257 plants were loss-making, accounting for 54.2% of the total number of plants, with a cumulative loss of 37.96 billion RMB, and an average debt-to-asset ratio of 88.6%。

Looking at individual enterprises, CHN Energy owns 152 coal-fired power plants with 170 GW of generation capacity, of which 77 are loss-making, with total losses of 11.32 billion RMB;China Huaneng owns 78 coal-fired power plants with 110 GW of generation capacity, of which 40 are loss-making, with total losses of 7.41 billion RMB.;China Datang owns 85 coal-fired power plants with 91.13 GW of generation capacity, of which 50 are loss-making, with total losses of 5.62 billion RMB;China Huadian owns 88 coal-fired power plants with 87.65 GW of generation capacity, of which 47 are loss-making, with total losses of 7.19 billion RMB;SPIC owns 71 coal-fired power plants with 67.89 GW of generation capacity, of which 43 are loss-making, with total losses of 6.42 billion RMB。

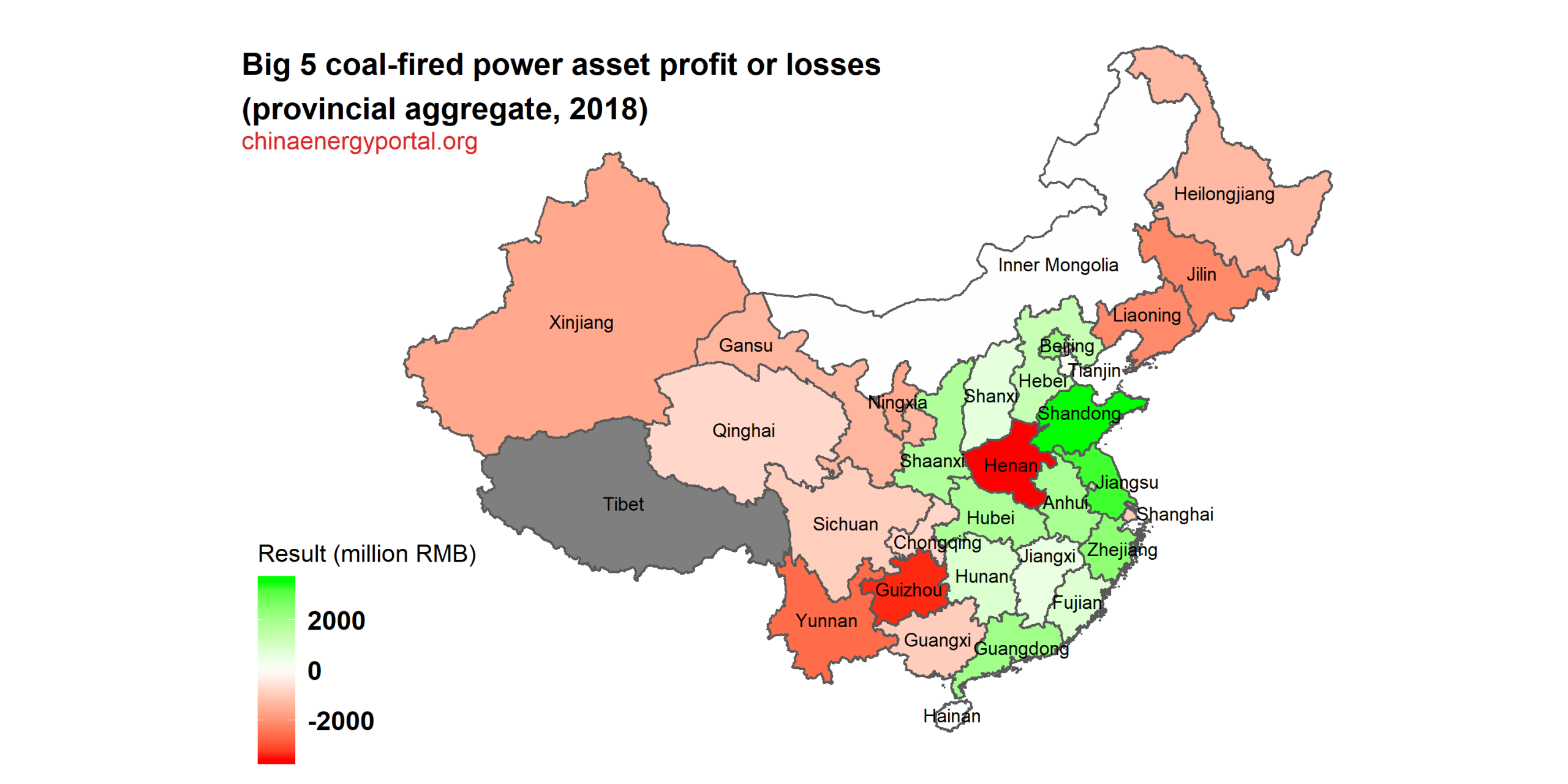

Looking at provincial-level administrative areas, coal-fired power assets of central government state owned power generation enterprises are mainly distributed over 30 provinces across the country:the coal-fired power assets of central government SOEs, when added together, generated a loss in 15 provinces in 2018, mainly in Northeast, Southwest, and Northwestern China, including Henan (-3.57 billion RMB), Guizhou (-3.4 billion RMB), Yunnan (-2.62 billion RMB), Jilin (-2.14 billion RMB), Liaoning (-2.13 billion RMB), Xinjiang (-1.62 billion RMB), Ningxia (-1.59 billion RMB), Gansu (-1.37 billion RMB), Heilongjiang (-1.33 billion RMB), Shanghai (-990 million RMB), Guangxi (-950 million RMB), Sichuan (-910 million RMB), Chongqing (-780 million RMB), Qinghai (-730 million RMB), and Inner Mongolia (-30 million RMB)。The coal-fired power assets, when added together, generated a profit in another 15 provinces in 2018, mainly in East, North and Southern China, including:Shandong (3.55 billion), Jiangsu (3.31 billion), Zhejiang (2.39 billion), Beijing (2.22 billion), Guangdong (2.08 billion), Anhui (1.93 billion), Hubei (1.81 billion), Shaanxi (1.77 billion RMB), Hebei (1.32 billion RMB), Hunan (860 million RMB), Fujian (810 million RMB), Shanxi (610 million RMB), Jiangxi (490 million RMB), Tianjin (220 million RMB), Hainan (40 million RMB)。

2. Objectives and basic principles

(i) Scope。These measures primarily target China Huaneng, China Datang, China Huadian, State Power Investment Corporation, and CHN Energy, but the scope may be expanded to other central government SOE with coal-fired power generation assets, such as SDIC, the China Resources Group, etc.。

(ii) Objectives。Starting in 2019, use circa 3 years to carry out trial measures for the integration of coal-fired power assets of central government SOE in key administrative areas. Through regional integration, optimize resource allocation, eliminate backward production capacity, reduce duplicative competition, ease operational difficulties, and promote healthy and sustainable development of the sector。Strive, by the end of 2021, to significantly improve the composition of production capacity in the trial areas, to continually increase the coordination of coal-fired power, to steadily improve operating efficiency, to reduce coal-fired power generating capacity by one quarter to one third, to significantly increase the average number of full-load hours for each generator, to reduce overall losses by more than 50%, and to significantly reduce debt-to-asset ratios。

(iii) Principles。

1. Adhere to the role of key industry actors。We will give full play to the central role of central enterprises in this regional resource integration and reform and escape from difficulties, and fully mobilize the initiative and creativity of enterprises by establishing fair and just, scientific and reasonable incentive and restraint mechanisms.。

2. Adhere to the role of the law and regulations。Increase awareness of the rule of law, promote the reorganization and replacement of coal-fired power resources and personnel transfer in accordance with laws and regulations, strengthen policy guidance, safeguard the equity of state-owned capital, and prevent the loss of state assets。

3. Adhere to comprehensive planning。Based on full consideration of regional characteristics and the specific situation of the enterprises, carry out the trial in batches at a time, advance the resource integration at a reasonable pace, ensure that trial measure work is progressing steadily, and generate results。

4.坚持维护稳定。在区域整合试点工作中坚持和加强党的领导,积极妥善处理资产、人员及债务等重大问题,牢牢守住不发生重大风险的底线,确保社会和企业的德定。

3. Key measures

(一)选择首批试点区域。在多次征求各企亚意见的基础上,将甘肃、陕西(不含国家能源集团)、新疆、青海、宁夏5个煤电产能过剩、煤电企业连续亏损的区域纳入第一批试点。

(二)明确区域牵头单位。原则上根据5家集困所在省级区域煤电装机规模、经营效益确定牵头单位,在此基础上,综合考虑地区电价、过剩产能消纳、煤电联营、各企业区域战略发展规划等因素,确定中国华能牵头甘肃,中国大唐牵头陕西,中国华电牵头新疆,国家电投牵头青海,国家能源集团牵头宁夏。

(三)稳妥开展资源整合。依法合规开展资产重组置换,以产权无偿划转为主,市场转让为辅,尽量不产生现金交易,人员、负债随资产一并划转。上市公司所属煤电企业,将股权上移至母公司后再划转,也可以市场化方式转让或置换。各企业划转资产总休平衡,差异较大的在以后试点批次中适当补偿。自备电厂、一体化项目、省级公司可不纳入整合,新建项目(不含即将投产项目)可暂缓纳入。

(四)淘汰关停落后产能。完成产权划转后,牵头单位要在保障供电供热安全的基础上,对达不到国家要求的煤电机组(含然煤自备机组)及符合地方淘汰标准的机组实施关停,坚决清理违规在建煤电项目。鼓励以市场化方式推进煤电过剩产能退出和低效无效资产处置。

(五)严格控制新增产能。属于国内电力产能预警红色和橙色等级的省区,自开展煤电资产重组起,原则上停止新建煤电投资项目、新增产能的煤电技术改追项目,确需新立项的项目需征得区域牵头单位同意。

(六)自觉维护市场秩序。加强区域经营协作,在综合考虑全部发电成本和资本合理回报水平的基础上理性报价,带头维护煤电市场正常秩序,自觉遵守交易规则,避免恶性竞争或恶性垄断,稳步有序推进电量交易市场化改策。

(七)加强管理技术协同。实现区域资产整合后,各牵头单位要围绕高质量发展,搭建统一的区域管理平台,避免各类重复性建设,强化内部人员、资金、管理、服务和产业协同,大力压缩可控成本费用,加快推进煤电业务减亏扭亏。要妥善解决试点区域内各企业职工收入不平衡问题,原则上收入水平不下降,逐步实现统一。

(八)推动企业转型升级。坚持绿色低碳的能源发展战略,加快燃煤发电升级与改造,努力降低供电煤耗、污染物排放,提高安全运行质量、技术装备水平,在试点区域带头打造高效清洁可持续发展的煤电产业。

(九)积极引入外部资本。牵头单位要通过债转股、引战投等措施加快降低试点区域煤电企业负债率,妥善化解债务风险,要积极探索混合所有制改革,完善现代企业治理,加快解决历史遗留问题,减轻包袱、激发活力,促进健康可持续发展。

(十)分步实施统筹推进。各企业要密切监测区域整合试点工作进展情况,积极协调出现的问题,及时总结经验教训,进一步完善资源整合工作机制,形成可推广的摸式,妥善推进下一批试点工作,力争2021年未全面完成.

4. Organizational safeguards

煤电资产重组置换工作涉及企业、金融机构、政府、员工等方方面面,政策性强、协调难度大,任务十分艰巨。各企业要切实把思想和行动统一到国资委的部署上来,勇于担当、主动作为,确保区域整合试点工作取得实效。

(一)建立工作机制。国资委成立由财管运行局、规划局、产权局、改革局、考核分配局、资本局共同参与的工作小纽,办公室设在财管运行局,统筹组织和协调工作。5家企业要在集团层面成立由主要领导牵头、有关部门参加的工作小组。各试点区域要成立由牵头区域主导、各涉及企业试点区域参与的工作小组,积极组织精干力量,确保责任层层落实。

(二)加强工作组织。各试点区域的牵头企业负责区域整合方案的制定和落实工作,要主动组织沟通协商,推动尽快达成一致意见,及时签订资产划转协议,明确划转的时问界限和双方贵任,其中人员、债务、安全等管理责任要随资产划转一并转移;要王动全面了解划入企业状况,做好接管工作,保证人员、安全等管理顺畅接续;要制定量化的管理整合目标和具体的保障措施,力争区域整合工作尽快取得实效。各试点区域参与企业要积极做好资源整合配合工作,及时提供反映电厂状况的财务数据等详细资料,对牵头企业提出的调研等工作任务和要求要及时回应,并给子必要的支持;要严格按照整合范围确定划转企业名单,并明确划转时点,避免遗漏,拖延和变更;耍充分做好资产登记、债务梳理、人员造册等管理权移交工作,确保划转工作顺利推进。

(三)制定工作方竟。各牵头企业要根据试点区域的装机情况、在建项目、资产债务等,与相关企业积极协商,充分研究,抓紧制定本战点区域整合工作方案,及时报送国资委。整合工作方案的内容主要包括:一是涵盖集团和区域2个层次的工作小组成员名单;二是划转企业清单,要列明划转时点;三是管理整合的目标和措施,要根据试点方案的总体目标制定牵头区域化解过剩产能、降低负债率和减亏扭亏的三年工作目标,并细化工作举措。

(iv) Strengthen policy support。经国资委批准,各企业对符合条件的划入煤电企业可以开展清产核资;因区域整合造成的资产、效益转移和清理淘汰落后产能造成的重大损失,国资委在业绩考核中适当考虑;对因资产重组对人员安置有重大影响或安置分流力度较大的,国资委在核定工资总额时予以适当考虑;在区域整合试点工作中涉及其他部门的事项,国资委积极子以协调,争取政策支持。

(五) 强化监督约束。国资委将对各企业制定的试点区域工作方案进行审核,并定期跟踪工作进展,加强对煤电资源区域整合试点工作的全过程监督检查,对进展缓慢、效果不佳的企业及时进行约谈提醒,同时,将煤电资源整侣试点工作推进情况作为企业考核. 监督.巡视和评价的重要内容,对工作不力、未完成整合目标的进行严肃处罚和追责。

Original scans of document as circulated on a number of Chinese websites: